The phrase “cashless hospitalization” sounds like a straightforward promise. You get admitted, the insurer pays the hospital, and you go home without having arranged a large sum of money at short notice. That promise is real, but the experience of actually living it out depends on details that most people never check until they are already sitting in a hospital admission queue.

What Cashless Health Insurance Actually Means

Let us start with the most important clarification: cashless does not mean free.

What it means is that for eligible expenses, your insurer settles the bill directly with the hospital rather than you paying first and claiming reimbursement later. The hospital still raises a bill. The insurer still reviews it. And there are usually some costs you will pay out of your own pocket, regardless.

These typically include any treatment not covered under your policy, items listed as non-payable in your policy document, any co-payment percentage your policy specifies, charges above your sum insured, and any room-related cost differences if you choose a room above your eligible category.

Understanding this from the beginning prevents one of the most common frustrations people experience during discharge, which is expecting a zero balance and discovering they owe a portion of the bill that the insurer does not cover.

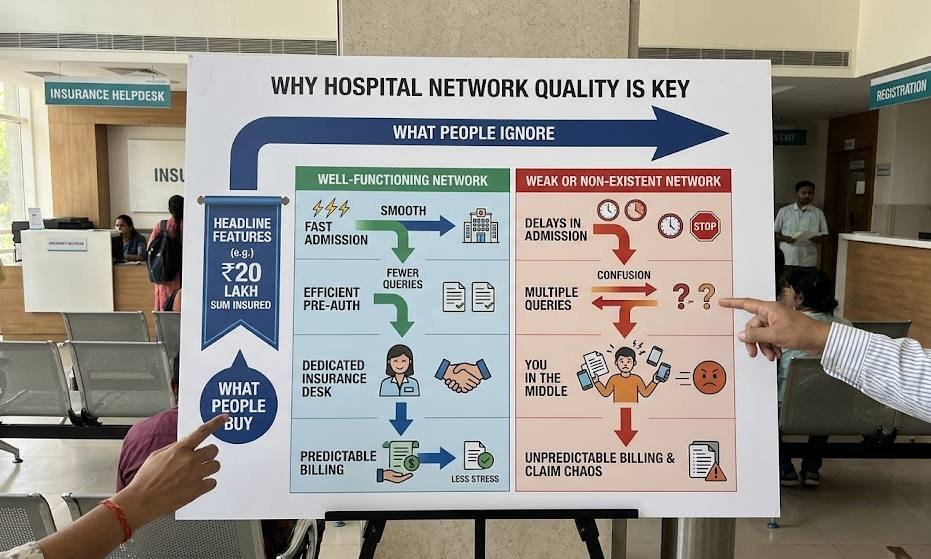

Why the Hospital Network Is the Part Most People Ignore

Here is something worth knowing before you buy a policy: the quality of your cashless experience depends less on the headline features of the plan and more on whether the hospital you need is part of the insurer’s network, and how well that relationship actually functions.

A network hospital is one that has a formal arrangement with the insurer or its Third Party Administrator (TPA) to process cashless claims. But not all network arrangements are equal. Some hospitals process dozens of cashless claims every week and have dedicated staff for it. Others are listed as network hospitals but rarely handle cashless cases and may not know the process well.

When you are choosing a health insurance plan, the size and quality of the hospital network in your city, your parents’ city, and any location where you realistically might need emergency care should be one of your primary filters, not an afterthought.

What a Strong Network Actually Looks Like in Practice

When a hospital has a well-functioning cashless arrangement with your insurer, the difference shows up in concrete ways during a hospitalization.

Admission moves faster because the hospital staff already know the process and exactly where to route your request. Pre-authorization, which is the insurer’s initial approval before treatment begins, tends to move with fewer delays because the hospital’s billing and medical teams understand what documentation is required and submit it correctly the first time. Billing at discharge is more predictable because the hospital follows agreed formats and package pricing. And when queries arise, the hospital has a dedicated insurance desk that handles them on a daily basis, rather than someone figuring it out for the first time.

When none of this infrastructure is in place, you end up in the middle of it, chasing approvals while managing your own or a family member’s treatment. It is a situation that is entirely avoidable with the right preparation.

Pre-Authorization Step: Why It Matters More Than People Realize

Pre-authorization is essentially the insurer’s green light before your treatment begins. The hospital submits your diagnosis, the proposed treatment plan, and an estimated cost to the insurer or TPA. The insurer reviews this, and either approves the cashless request, queries it for more information, or partially approves it.

This step is where many cashless experiences either go smoothly or start to unravel.

If the hospital submits an incomplete request, perhaps missing clinical notes or submitting a vague diagnosis, the insurer will raise queries. Those queries take time to resolve. Meanwhile, you are already admitted and anxious about what is happening. If the initial approval is for a lower amount than the actual cost, the hospital may ask you for an interim payment while the enhanced approval is processed.

What You Can Do to Help the Process Along

You do not have to be a passive participant in pre-authorization. A few simple steps make a genuine difference.

When you are admitted, ask the hospital to confirm that a pre-authorization request has been raised and ask for the reference number. If your treatment plan changes, such as an additional procedure becoming necessary or a longer stay being recommended, ask the hospital to submit an enhancement request promptly rather than leaving it until discharge.

Keep your insurance e-card and a valid photo ID with you at admission and hand them over without waiting to be asked. The sooner the hospital has your details, the sooner the process begins.

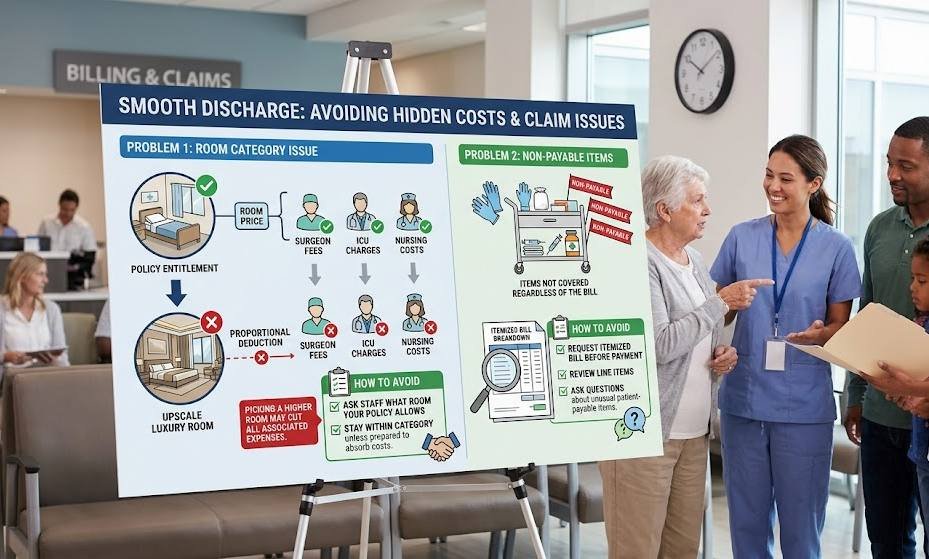

Common Problems at Discharge and How to Avoid Them

Discharge is often where the stress of cashless claims is most concentrated, and it is usually avoidable.

Room Category Issue

This is one of the most common sources of unexpected bills. Most health insurance policies link your room entitlement to a specific category, such as a single private room or a room up to a certain daily rent. If you choose a room above that category, it does not just mean you pay the difference in room rent. Many insurers apply a proportional deduction across associated expenses, including surgeon fees, ICU charges, and nursing costs, because these are calculated as multiples of room rent in hospital billing systems.

The practical advice here is simple: before choosing your room, ask the hospital admission staff which room category your policy allows and stay within it unless you are fully prepared to absorb the additional costs.

Non-Payable Items

Every health insurance policy includes a list of items the insurer will not pay for, regardless of whether they appear on a hospital bill. Common examples include surgical gloves, cotton, syringes, certain dietary supplements, and administrative charges. This is not unique to one insurer; it is a standard feature of most policies in India.

Ask for an itemized breakdown at discharge and review it before paying. If something on the patient-payable list seems unusual or has not been explained, ask for clarification before signing off.

How to Check If a Hospital Network Is Right for You Before You Buy

Most people look at a hospital network list and simply count hospitals. A more useful approach is to check for quality and relevance.

Ask yourself these questions before committing to a policy:

Are the hospitals you already use, and the ones closest to where you and your family live, included in the network? Does the list include hospitals with the specialities you are most likely to need based on your age or health history? Do the listed hospitals have a dedicated insurance or TPA desk, or is cashless handled by general admin staff? Is there clarity on how emergencies are handled, specifically whether cashless can be processed even if admission happens outside business hours?

Most insurers publish their network hospital lists online, and you can call individual hospitals to ask how frequently they handle cashless claims and whether they have dedicated support for it. This five-minute check before buying a policy can save significant stress later.

Real-Life Situations Where Cashless Claims Go Wrong

Consider a family in Pune whose father was admitted to a hospital listed in their insurer’s network. The hospital had never actually processed a cashless claim before and did not have an insurance desk. The billing team submitted an incomplete pre-authorization request, the insurer raised multiple queries, and by the time approval came through, the family had already paid out of pocket to avoid delay. The reimbursement process then took months.

This situation is not rare. It happens specifically because people assume “network hospital” means “smooth cashless experience” without verifying the hospital’s actual familiarity with the process.

A parallel situation in planned hospitalization involves elective surgeries booked in advance. When a patient in Chennai scheduled a knee replacement at a private hospital that had an active insurance desk, the pre-authorization was submitted a week before admission, queries were resolved in advance, and the admission itself was largely paperwork-free. The difference was entirely in the hospital’s experience with the cashless process.

A Practical Checklist for Your Next Hospitalization

Whether you are being admitted for a planned procedure or in an emergency, these steps reduce friction and prevent surprises:

Carry your insurance e-card and photo ID at all times when hospitalization is likely. Share them at the admission desk immediately without waiting to be prompted. Confirm the pre-authorization reference number before treatment begins. Verify your room category entitlement and choose accordingly. If your treatment plan changes, ask the hospital to raise an enhancement request the same day. At discharge, ask for an itemized bill and a clear explanation of what is being charged to you as the patient-payable portion. Do not pay until you understand every line item and agree it is correct.

Bigger Picture: Why This Matters for Your Health Decisions

Managing a medical situation is stressful enough on its own. Having to navigate insurance paperwork, chase approvals, or arrange emergency funds while someone you love is unwell adds a layer of difficulty that proper preparation can largely eliminate.

The right health insurance plan is not just the one with the lowest premium or the highest sum insured. It is the one that will actually work for you when you need it, in the hospital you trust, with a claims process that does not add chaos to an already difficult moment.

Do the homework before you buy. Verify the network. Understand your room entitlement and co-payment terms. And when hospitalization happens, stay slightly ahead of the paperwork rather than reacting to it.

References

- Insurance Regulatory and Development Authority of India. Master Circular on Health Insurance Business 29052024. Reference No. IRDAI/HLT/CIR/PRO/84/5/2024. Hyderabad: IRDAI; 29 May 2024.

- Insurance Regulatory and Development Authority of India. IRDAI (Health Insurance) Regulations, 2016. Reference No. F. No. IRDAI/Reg/17/129/2016. Hyderabad: IRDAI; 29 July 2016.

- Insurance Regulatory and Development Authority of India. IRDAI (Third Party Administrators – Health Services) Regulations, 2016. Reference No. F. No. IRDAI/Reg/5/117/2016. Hyderabad: IRDAI; 28 March 2016.

- Insurance Regulatory and Development Authority of India. Modification of Existing Format for “Request for Cashless Hospitalization”. Circular Reference No. IRDA/HLT/REG/CIR/86/05/2019. Hyderabad: IRDAI; 27 May 2019.

- Insurance Regulatory and Development Authority of India. Guidelines on Standardization of Exclusions in Health Insurance Contracts. Circular Reference No. IRDAI/HLT/REG/CIR/177/09/2019. Hyderabad: IRDAI; 27 September 2019.

- General Insurance Council. Press Release: Launch of “Cashless Everywhere” by General Insurance Council. Mumbai: General Insurance Council; 24 January 2024.