Choosing a dental plan often starts with monthly cost, but that should never be the only factor. Many people sign up for coverage expecting help with a wide range of services, then later learn that some treatments are limited, delayed, or not covered at all. That is why it helps to review exclusions before enrolling.

For patients comparing options, the real question is simple. What does the plan help pay for, and what costs may still fall on you?

Why Exclusions Matter Before You Choose a Plan

Dental coverage can look appealing at first glance because many plans include preventive care and some support for basic and major services. Preventive services are often emphasized, while other services may come with limits, waiting periods, or reduced coverage.

That matters because a plan is only useful if it matches the care you expect to need. Someone looking for help with cleanings and exams may have a very different experience from someone expecting support for crowns, dentures, implants, or orthodontic treatment. Reading the exclusions first can prevent frustration later.

Which Services Are Commonly Left Out

One of the biggest issues in dental coverage is that not every procedure is treated the same. Cosmetic treatments such as teeth whitening are commonly excluded, and orthodontic procedures may also be excluded unless a specific policy includes them.

Implants and other costly treatments may not be fully covered, and some services may only receive partial support when medical necessity can be shown. In practical terms, that means patients should not assume a treatment is covered simply because it is dental care. The details often depend on the exact policy.

Another area that can be confusing is replacement work. Some plans place limits on how often crowns, dentures, bridges, or other major restorations can be replaced. A patient may assume a damaged appliance will be covered right away, only to find that the plan requires a set number of years between replacements. That can lead to higher out-of-pocket costs when dental work wears down sooner than expected.

Patients should also pay attention to procedures related to pre-existing issues or ongoing treatment plans. In some cases, a plan may restrict coverage for work that began before enrollment or for procedures considered optional rather than necessary. Even when a service is not fully excluded, it may be covered at a lower percentage than expected.

This is why reading the exclusions list matters so much. It gives patients a clearer view of what the plan may actually help pay for and where they may still need to budget for treatment on their own.

How PPO Rules Can Still Lead to Higher Costs

Aetna plans may offer flexibility through a PPO structure, but flexibility does not always mean low cost. Members may use out-of-network providers, though doing so may result in higher out-of-pocket expenses. Annual maximums are also common, which means coverage can stop once the plan reaches its yearly payment cap.

That combination can create a gap between what patients expect and what they end up paying. A routine year with preventive care may be manageable, but a year involving several larger procedures can become more expensive if annual limits are reached quickly.

Why Waiting Periods Should Not Be Overlooked

Another point patients often miss is timing. Preventive care may have no waiting period, but major procedures can require members to wait months before coverage begins.

This can be a problem for anyone who expects treatment soon after enrolling. If you already know that you may need dentures, root canal treatment, crowns, or other larger services, it is worth checking when coverage begins and whether any restrictions apply during the first policy year.

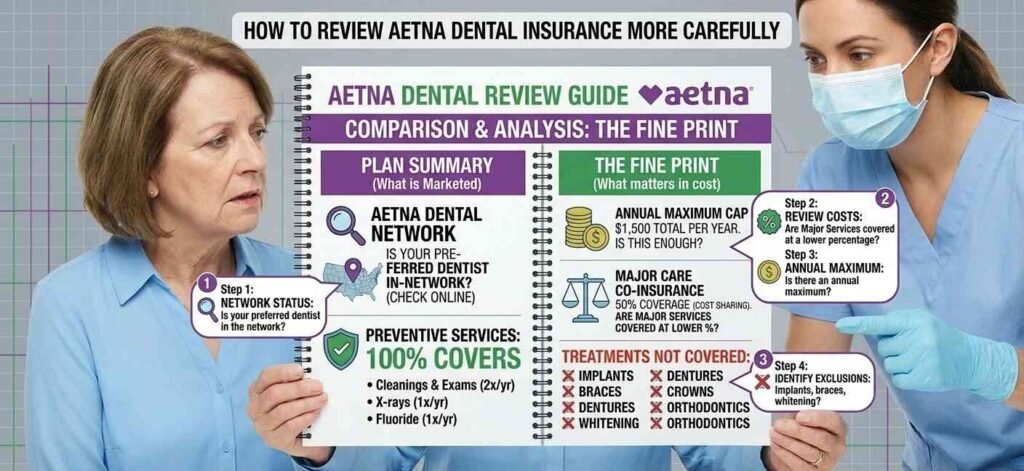

How to Review Aetna Dental Insurance More Carefully

When comparing Aetna dental insurance, patients should read the summary of benefits with a few specific questions in mind. Is your preferred dentist in the network? Which preventive services are covered? Are major services covered at a lower percentage? Is there an annual maximum? Are implants, braces, whitening, or other treatments excluded?

This step matters because broad marketing language can make plans sound similar when the real differences lie in exclusions and cost sharing.

What Patients Should Keep in Mind Before Enrolling

Dental coverage works best when expectations match the policy. Aetna plans may support preventive care and some restorative treatment. Still, exclusions for cosmetic services, limits on certain major procedures, annual maximums, out-of-network costs, and waiting periods can all shape the final value of the plan.

Before enrolling, patients should compare what they need now, what they may need later, and what the plan may leave unpaid. That kind of review can make it easier to choose coverage with fewer surprises and a better fit for long-term dental care.

Frequently Asked Questions (FAQs)

1. Does Aetna dental insurance cover cosmetic dental procedures?

- Most dental insurance plans, including many Aetna policies, do not cover cosmetic procedures. Treatments such as teeth whitening, veneers, or purely aesthetic improvements are typically excluded because they are not considered medically necessary. However, some procedures that improve both appearance and function may receive partial coverage depending on the policy details.

2. Are dental implants covered under Aetna dental plans?

- Coverage for dental implants varies by plan. Some Aetna policies may partially cover implants, while others may exclude them completely or only cover alternative treatments, such as bridges or dentures. It is important to review the specific plan’s benefits summary to understand whether implant procedures are included and what portion of the cost may be covered.

3. Do Aetna dental plans have waiting periods for major treatments?

- Yes, many dental insurance plans include waiting periods for major procedures. Preventive services like cleanings and exams may be available immediately, but treatments such as crowns, root canals, or dentures often require members to wait several months before coverage begins. The exact waiting period depends on the plan.

4. What is an annual maximum in dental insurance?

- An annual maximum is the total amount a dental insurance plan will pay for covered services within a calendar year. Once that limit is reached, any additional treatment costs must be paid by the patient. Understanding the annual maximum can help patients estimate potential out-of-pocket expenses if they require multiple procedures in the same year.

5. Can I see any dentist with an Aetna PPO dental plan?

- Aetna PPO plans usually allow members to visit both in-network and out-of-network dentists. However, visiting an in-network provider typically results in lower costs because negotiated rates apply. Choosing an out-of-network dentist may lead to higher out-of-pocket expenses.

Final Thoughts

Dental insurance can be a helpful tool for managing routine care and reducing the cost of certain procedures. Still, it is important to understand that not all treatments are covered equally. Reviewing exclusions, waiting periods, provider networks, and annual maximums before enrolling can help prevent unexpected expenses later.

By carefully comparing plan details and considering your current and future dental needs, you can choose coverage that better aligns with your expectations and long-term oral health goals. Taking the time to review these details ensures that your dental insurance serves as financial support rather than a source of unexpected costs.

Disclaimer

This article is provided for informational purposes only and should not be considered financial, insurance, or medical advice. Dental insurance coverage, exclusions, waiting periods, and benefits may vary depending on the specific policy, provider, and location. Individuals should review official plan documents or consult directly with the insurance provider or a licensed insurance professional to obtain accurate and up-to-date information about dental coverage options.